Date: 03 December 2020

Author:

Rob Lincolne, Founder and CEO,

Paydock

“In New York, freedom looks like too many choices.” U2

Revolut, Monzo and the endless stream of wallets, buy-now-pay-laters, loyalty, crypto and alternative payment methods have, in recent years, been defining monikers of fintech. Yet, as fintech enters its adolescence, the next generation of its success will not come from anodised aluminium cards, slightly better interest rates or bio-authentication alone.

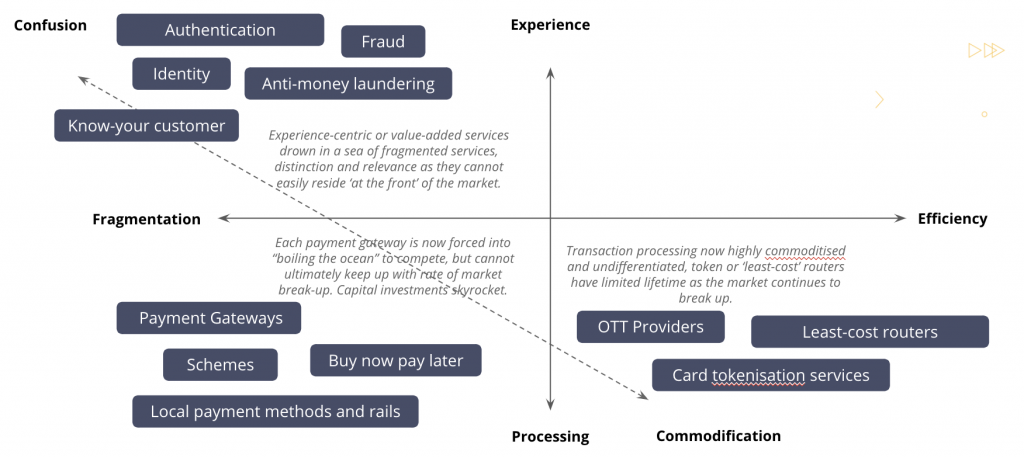

Fintech 3.0 is B2B – providers who focus on tangible value and address vital needs across organisations of all shapes and sizes by returning genuine, immediate bottom line value in challenging days. In a sea of undifferentiated, fragmented fintech choice, merchants have become a driving force behind capital markets who themselves recognise the shift in the wind as the industry focuses on margins, returns and the core of commerce. B2B fintechs will operate out of a driving mission to solve fundamental, operational and systemic challenges in a complex fintech world and help merchants capitalise (rather than drown) in today’s boiling ocean of fintech choice. B2B fintech is ready for prime time.

The pace of fragmentation and commoditisation across the B2C fintech space has been well documented through the rear-view mirror. Now at a tipping point, the value gap has presented what now constitutes a greenfield opportunity to restore balance to the fintech world. This new phase of fintech as noted by

Cornerstone advisors, is already underway as

“investors’ focus is beginning to move away from business-to-consumer (B2C) fintech”.

An

article by Forbes further paved the way for this contemporary understanding of a) exactly what B2B fintech is, and b) why it is the new focus of smart money. This shift and transition in investor appetite towards B2B fintechs is also recognised in the latest Dealroom data which indicates that European funding is now more heavily focused on B2B fintechs. As challenging this year may have been, European fintechs raised €5bn across 373 deals during 2020 alone. With continued uncertainty and the prospect of global slowdown as a result of the pandemic, B2B – although not entirely immune from the impact of pandemic – is undoubtedly a safe haven for investors looking for tangible value, margins and operational efficiency.

The B2C market will continue to grow, especially in emerging economies. Consumers have been quick to respond (or at the very least, experiment) even while loyalty is low – and merchants have to some degree been left behind the curve. Their challenge? Embracing a generation of fast-paced millennials now operating on payment rails never seen before.

The unintended consequence of all this B2C fintech mayhem (another morning, another pay-with-something) is that merchants face two problems. First, they can no longer easily differentiate across a commoditised processing market (Stripe is now one of many). Secondly, they must identify a way to consume and support/manage localised and specialised services (consider the cohort of Afterpay competitors entering the market, let alone faster/realtime banking and transactional platforms). Administration, technical and data costs skyrocket, and agility slows.

Services like Stripe and others have also, at great cost, demonstrated that while B2C service velocity increases, boiling the ocean also becomes a challenge. As margins are compressed, merchants actively seek for ways to leverage their buying power and exploit the race to the bottom. One simple example is that of schemes and acquirers rising up from underneath the gateway partners and cutting out ‘the middleman’. The race intensifies daily.

Further analysis of the industry also identifies a number of specialised providers who deliver value across the payment function, capitalising on technologies such as machine learning and artificial intelligence.

The future of fintech therefore depends on ensuring merchants can easily capitalise on this rich field of B2C fintech value. In much the way we’ve seen Amazon make it easy for consumers to capitalise on a broad market of consumer products, the next wave of B2B fintechs will be focused on making it easy for merchants to capitalise on the rich playing field of financial services.

If Fintech 2.0 was about the consumer, Fintech 3.0 starting in 2020 will undoubtedly be about the merchant.

Rob Lincolne is a global entrepreneur with extensive experience in payments industry for over 10 years. He is the founder and CEO of PayDock, a sophisticated payments orchestration platform for the not-for-profit organisations, medium to large online merchants, fintechs and banks.

Rob specialises at creating payments acceptance strategies for the modern merchant and has successfully designed and developed solutions for Tier 1 NFPs in Australia, one of China’s largest banks, a large Australian Supermarket chain and a well-funded UK POS Startup.

Rob founded PayDock in 2015 having previously co-founded and run a successful digital marketing agency for 11 years, working closely with not-for-profit organisations and learning the real pain points NFPs are facing today: online payments. It was this insight that prompted him to build PayDock.

Rob’s goal today is to retrieve billions of trapped dollars, drive financial inclusion as well as bring innovation to the status quo of online payments across the globe. The sky is his limit.

As PayDock’s CEO, Rob is responsible for the overall business strategy and growth and the manifestation of PayDock’s company values in every part of the business, which are close to his heart: Opportunity, Stewardship, Beauty and Mastery.

Rob Lincolne is a global entrepreneur with extensive experience in payments industry for over 10 years. He is the founder and CEO of PayDock, a sophisticated payments orchestration platform for the not-for-profit organisations, medium to large online merchants, fintechs and banks.

Rob specialises at creating payments acceptance strategies for the modern merchant and has successfully designed and developed solutions for Tier 1 NFPs in Australia, one of China’s largest banks, a large Australian Supermarket chain and a well-funded UK POS Startup.

Rob founded PayDock in 2015 having previously co-founded and run a successful digital marketing agency for 11 years, working closely with not-for-profit organisations and learning the real pain points NFPs are facing today: online payments. It was this insight that prompted him to build PayDock.

Rob’s goal today is to retrieve billions of trapped dollars, drive financial inclusion as well as bring innovation to the status quo of online payments across the globe. The sky is his limit.

As PayDock’s CEO, Rob is responsible for the overall business strategy and growth and the manifestation of PayDock’s company values in every part of the business, which are close to his heart: Opportunity, Stewardship, Beauty and Mastery.

Join Paydock and other industry-changing fintechs in the FINTECH Circle startup community.

Find out more.