Date: 24 August 2025

Author: Gaya Chandrasekaran

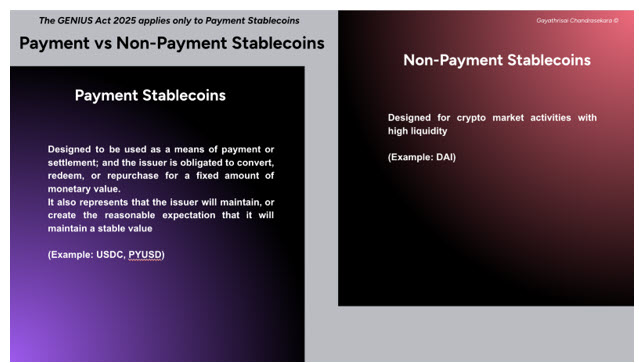

The GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act) is a U.S. federal law signed in July 2025 that creates the first comprehensive regulatory framework for payment stablecoins.

Read on to discover what the Genius Act is and more about Assets tokenisation

Larry Fink, the chairman and CEO of BlackRock, said in January 2024: “We believe the next step going forward will be the tokenization of financial assets, and that means every stock, every bond … will be on one general ledger.”

The “GENIUS Act” in a Nutshell

- The Act defines payment stablecoins as digital assets issued for the purpose of payment or settlement (including margin/collateral), redeemable at a fixed value (e.g., $1), backed 1:1 by permitted reserve assets and does not offer a payment of yield or interest.

- It outlines requirements for issuers around reserve composition, usage restrictions, redemption & disclosures as well as risk oversight.

- Stablecoins may be issued by Subsidiaries of insured depository institutions (IDIs), OCC-regulated nonbank entities (to start under local laws and migrate to federal oversight when issuance >$10bn), State-regulated entities (<$10bn in issuance). A non-US issuer can still trade on US secondary markets under certain conditions.

- Issuers are expected to have technological capability that embraces transfer freezes or reversals under compliance or court orders, AML/sanctions screening and reporting capabilities as well as annual certifications confirming they meet AML program standards.

Let us understand a bit about tokenized money before exploring what the Act means for Asset Tokenization.

Tokenized Money

Over the past few years, central banks and financial institutions have created several types of tokenized money. These include the following:

- Central bank digital currencies (CBDCs) are the official digital version of a fiat currency. It is considered as legal tender backed by the central bank and issued on a permissioned ledger (though not publicly accessible). CBDCs can be for retail use (public) or wholesale (for B2B settlement).

Examples include the People’s Bank of China’s e-CNY and the Eastern Caribbean Central Bank’s DCash (EC Dollar).

- Stablecoins are tokenized cash issued by private institutions on public blockchains (for example, Ethereum), pegged to fiat currency, and backed by audited reserves. They are not legal tender and have been the recipient of varying levels of regulatory scrutiny and oversight.

Examples include Tether (USDT), Circle (USDC), and EUR CoinVertible (EURCV).

- Tokenized Deposits (Bank-issued) are tokenized representations of customer deposits in bank accounts, backed one-to-one by funds held by the issuing institution. The main purpose of these tokens are to enable real-time payments and settlements involving institutions (intra or inter).

One example is JPMorgan’s JPM Coin.

Tokenized deposits hold an existing bank liability in a cryptographic shell; the token inherits deposit insurance, Basel capital and lender‑of‑last‑resort support. Stablecoins being obligations of a non‑bank issuer, circulate on public chains and are secured by segregated reserves, usually short‑dated Treasuries.

Regulators have historically preferred the first model (for its guard-rails) whilst markets have favoured the latter (for its unrestricted liquidity). However, the GENIUS Act is expected to bring regulatory credibility to the latter, of course only to the ones that comply with the provisions of the act.

Why Tokenized Money?

- These are used to clear funds and settle payments almost instantly, requiring verification of existing funds and confirmation of sending/receiving entities before a transaction can be initiated.

- Digital compliance processes and smart contracts aid automatic AML/KYC/Sanctioned Entities checks via on-chain analytics services.

- These types of money challenge the traditional global payments rails, such as utilizing the Swift payment messaging network, using correspondent banking, or employing wire transfers such as Fedwire.

- According to data from Swift and Bank for International Settlement (BIS) existing legacy payments infrastructure processes around $5-7tn in global transfers daily. In contrast, Sablecoins facilitate only about $20-30bn of on-chain payment transactions per day (less than 1% of global volume). However, if the growth of volume of stablecoin transactions over the past few years were to sustain, they could surpass legacy payment volumes in less than a decade. The key traits of tokenized cash (to operate continuously, satisfy demand for instant settlement, and offer improved operational risk controls solves real-world pain points) offer a compelling value proposition for wider adoption.

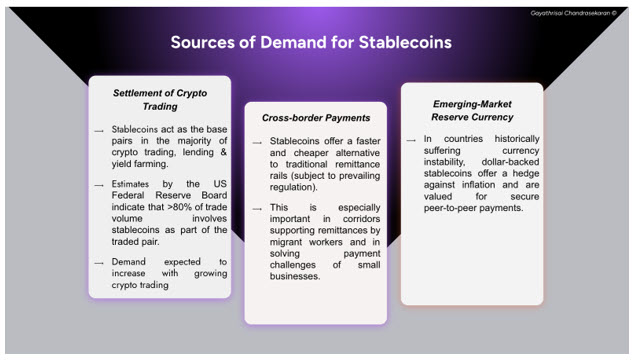

Stablecoin Uses

Popularity of Stablecoins stems from their speed, availability (24×7), inclusion (larger sections of the population underserved or excluded by KYC regulations have access), transparency and lower cost.

Stablecoins are used in settlement of crypto trading, cross-border payments and emerging market reserve currency.

About the Author

Gaya Chandrasekaran is a Senior Banker with over 17 years of experience across corporate and investment banking at leading global financial institutions. Her expertise spans client origination, bespoke financing structures, and strategic advisory, with a deep sector focus on fintech and technology.

She completed her Masters in Finance from London Business School and an MBA from India.

An active contributor to the LBS alumni community, Gaya has held several leadership roles, most recently serving as Co-President of the Alumni Tech & Media Club, helping foster engagement at the intersection of finance, technology, and innovation.

Outside of banking, Gaya is also an accomplished contemporary artist known for her textured acrylic landscapes. Born in the coastal city of Chennai, India, her artistic practice is influenced by the vivid colors and rich cultural heritage of her upbringing. Her disciplined, detail-oriented approach—shaped by years in banking—translates into precision-driven, tactile artworks. She has trained in India and at the Slade School of Fine Art in London.

Her work has been exhibited across London, Europe, the USA, and Asia, with features in publications such as the Contemporary Art Curator, Artist Close Up, and Artist Talk Magazine. Her paintings are held in private collections across the US, UK, Spain, Brazil, and India.

“Please note the opinions expressed within the content above are solely the author’s and do not reflect the opinions and beliefs of people, institutions, or organisations that the owner may or may not be associated with in a professional or personal capacity.”