Date: October 10 2025

Author: FINTECH Circle

Around 1.7 billion people globally remain unbanked, and millions more are underbanked—unable to access the full suite of financial services needed to build a secure future. This isn’t just a developing world issue—it’s happening in major economies too, including the UK, where nearly a million adults still don’t have a bank account.

This blog summarises the depth of the conversation—covering global challenges, real-world examples, innovation use cases, and a live Q&A that addressed everything from regulation to crypto, investor sentiment, and scaling inclusive fintech solutions.

Defining Financial Inclusion – More Than Just Access

Meaghan Johnson opened the discussion by setting the foundation:

At its core, financial inclusion is about access—specifically, ensuring that individuals and businesses can use affordable, useful and responsible financial services. Drawing from the World Bank definition, Meaghan highlighted that true financial inclusion goes beyond opening bank accounts—it must be sustainable and meaningful.

She unpacked three layers of barriers that prevent people from engaging with the financial system:

1. Level: State/National

Barriers: Weak digital ID systems, lack of financial infrastructure, poor policy frameworks

2. Level: Private Sector

Barriers: Limited investment in underserved segments, outdated distribution models

3. Level: Individual

Barriers: Low financial literacy, mistrust, lack of proximity to financial services

Meaghan also clarified two key categories of exclusion:

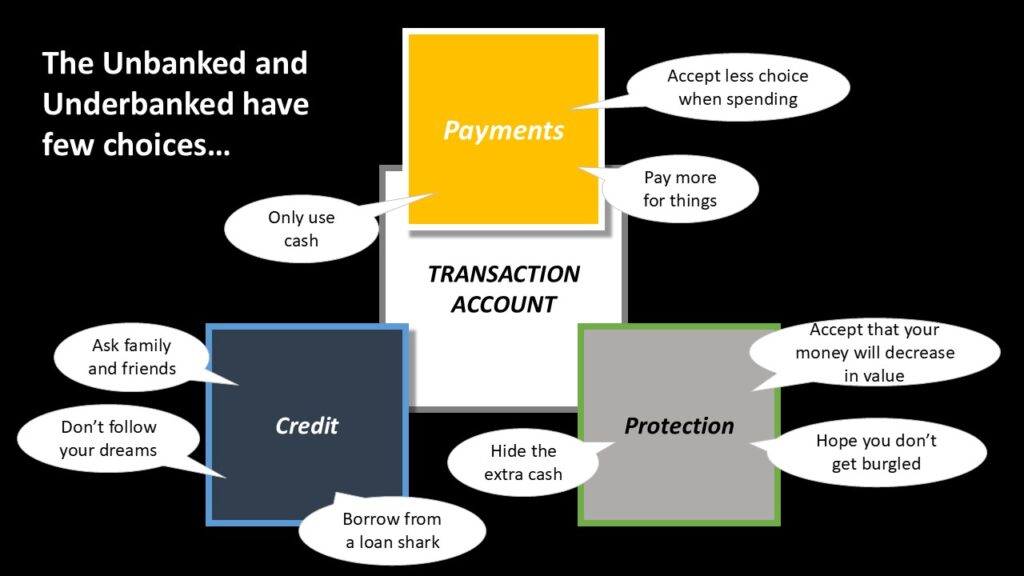

- Unbanked: No access to any formal financial services

- Underbanked: Have limited services but lack full access to savings, loans, insurance, or investments

Despite challenges, she noted positive momentum—global financial exclusion is slowly shrinking, largely due to digital financial services and mobile money.