Event: FINTECH Circle Autumn Drinks 2025

Date: 30th September 2025

Author: FINTECH Circle

September meant it was time for our Annual FINTECH Circle “Autumn Drinks” which brought together our community of leading Fintech entrepreneurs, investors, and financial services professionals from across the UK.

More than 72 guests came together for an evening of Fintech discovery, networking, sharing ideas, making friends and looking for partnerships to scale up their businesses. The event was hosted by our partner, MHA , a trusted advisor to ambitious FinTech

companies.

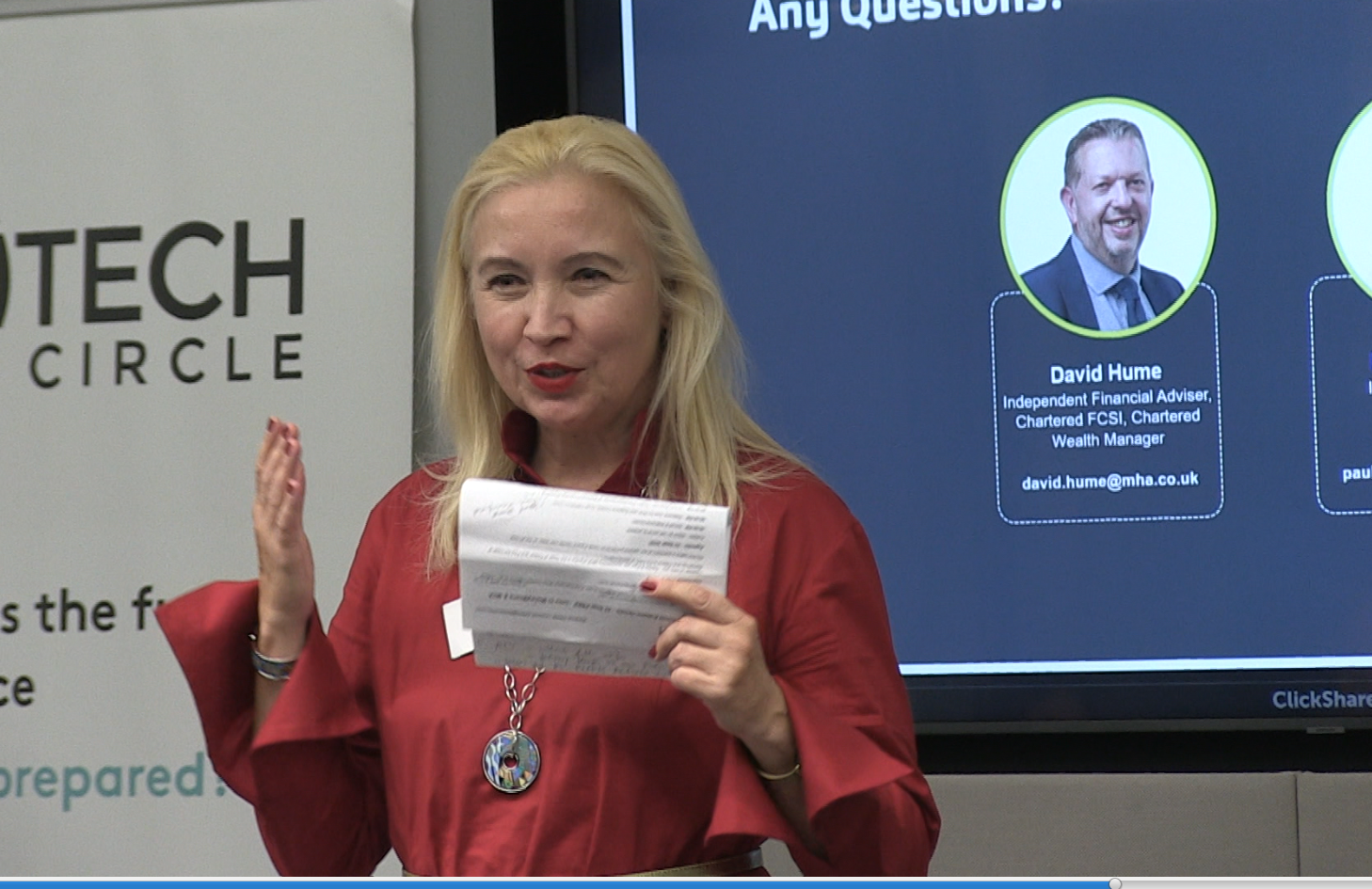

After the initial welcome drinks, FINTECH Circle’s Chair Susanne Chishti opened the evening, followed by keynotes from David Hume, an Independent Financial Adviser and Chartered Wealth Manager at MHA and Paul Mansfield, an Investment Manager and Chartered FCSI, also from MHA.

A panel discussion followed with:

- Helena Wardle, Founder of Money Means

- Chris Blundell, Partner at MHA

- Susanne Chishti, Moderator and Chair of FINTECH Circle

Keynote – David Hume:

David began by telling us all about MHA, which is the UK member firm of the global Baker Tilly International network, with over 2,000 UK-based employees. David explained that MHA Wealth is part of MHA and operates across the MHA UK office network.

As an independent financial adviser (IFA) working at MHA Wealth, David explained that MHA is one of the few firms that offer integrated financial planning, wealth management, tax advice, and audit services. This broad range of advice is perfect for clients who appreciate the benefits of a wrap-around service to deliver an optimum tailored solution for wealth management and tax planning in particular. It has also helped MHA to share best practices and IT investment to support client work.

David went on to discuss how MHA is trialling AI for selected processes to offer a superior service, working with companies such as Saturn and Aveni, which specialise in AI development for the wealth management sector, amongst others. MHA has also been using an innovative cash flow modelling tool, which brings clients’ wealth and planning to life, as well as using the Moneyinfo app to support client management. This all means that MHA is committed to not just providing advice but constantly seeking ways to deliver a superior service to its clients.

Despite all the technology, David explained his expertise is focused on a personal approach and providing holistic independent financial planning. He has been advising clients for over 35 years, but during that time with all the changes in legislation the one thing that has never changed is that no one lives forever, or as David put it:

“If you take nothing else from today’s presentation, please take some time out to sit down and consider your position. What would be the situation for your family if you were to die? How would they cope? And also, very importantly, what would happen to your business?”

MHA specialises in helping clients to navigate all stages of their lives through independent unbiased advice. David discussed several protection options worth considering:

“Not many business owners have heard of a Relevant Life policy… that’s your own life cover for your family which is written in trust. However, your company pays the premiums, and it will end up costing you around 50%, of the equivalent personal life policy after all the tax savings.

So, if you have a business and you have the ability and the funds to pay for life cover for the senior employees, yourself, or maybe someone else, it’s a big benefit for you to consider.”

He also discussed:

“You also must consider what impact the death of a key person would have. That maybe you or that may be one of your colleagues.

If you died, it may be the receptionist who has all the contacts. Whoever that keyperson is, what impact will that have, that death, on the business?

Will it continue to be able to run?

Will the profitability be significantly impacted?

Also, as a shareholder. What shareholder agreement do you have in place if you have other shareholders apart from yourself?

Will your partner or spouse receive value on your death?

Who would inherit the shares and potentially, could they pay the inheritance tax due or be forced to sell them to a third party?

Would you want to be sitting and running a business with the new third party in the

future?”

David explained you can organise policies which would ensure you have liquid assets to be able to pay inheritors the value of the shares.

He also mentioned if you have your own company, you can contribute to a pension up to the annual allowance of £60,000 per annum. And even if you’re paying yourself a nominal salary, such as £10,000 or £12,000, you can still pay from the business a contribution of £60,000 as part of your overall remuneration package into your pension.

So, although pensions have been in the news quite a bit lately, as they are coming into scope for IHT, they are still one of the most tax-efficient ways of withdrawing money from the business for your future benefit. Other tips included:

“…It is important to review any existing plans you have at the moment, beyond protection and retirement planning, so also think about tax efficient saving.”

David explained that as he is an advisor, he can provide advice on all the different types of investment structures. These can include ISAs as a starting point or individual savings accounts.

“…If you’re not using those at the moment, you can save up to £20,000 a year. I would encourage you to consider these if you have cash savings available.”

However, because pensions are now so restricted, people are looking at alternative investment structures such as venture capital trusts (VCT), enterprise investment schemes (EIS), or seed enterprise investment schemes (SEIS) as well. David can advise clients on all these types of investment, but they do come with a health warning. They are considered higher risk investments; however, you do normally benefit not only from 30% tax relief, but also from other tax benefits as well.

“Some of you in the room may be looking at investments in VCT and EIS companies. Chris Blundell will be talking about those investment opportunities, especially where attracting, rewarding, and keeping employees is concerned.”

Finally, David told our audience that it’s essential to plan for a business sale. He advised NOT to leave it until the last minute and get a good team working with you in the early days. How you structure your remuneration before the sale can affect the sale price, so it’s important to look at how you will have sufficient funds to live on from the sale. MHA Wealth can assist with cash flow modelling to show you how long your wealth would last.

Keynote: Paul Mansfield

Next, we heard form Paul Mansfield, Investment Manager and Chartered FCSI at MHA

Wealth.

Paul spoke about how he could assist the audience in building wealth over time.

Paul told the audience:

“We run two services. There is a bespoke discretionary service and a model portfolio service.”

He explained:

“…The market is split between model portfolio services and multi-asset open ended investment companies, and more traditional bespoke investment management services.

Model portfolio services are a one-size-fits-all approach. They don’t have personalisation, but they’re effectively an investment manager’s best ideas at very low cost, typically 0.25%.”

He discussed that MHA also offers a bespoke, tailored service. This involves a much more personalised strategy for individuals and there are often tax implications to consider.

“Lots of clients have ethical preferences, specific income requirements, or they need to balance their risk in portfolios for a variety of different reasons, which I’ll touch on in a moment.”

Paul illustrated the situation of a tech entrepreneur (obviously leaning towards the audience here) who has a lot of money tied up in their personal private company and they are in need of diversification, a lot of risk concentrates in one area, and MHA tailors portfolios to manage that risk.

“…So we will introduce strategies and asset allocation, in order to dampen risk in their portfolio, so they are less risky in their personal life. In fact, we often find people, entrepreneurs by nature, seem to want to continue to press that risk, and we often build up portfolios that have more tech in than they originally had, but that would be one example.”

MHA has a strong process for building our tactical asset allocation, positioning and portfolios. Paul touched on MHA’s sentiment and positioning with the portfolios, mainly because that’s what everyone enjoys hearing about.

“So in essence, we know as investors and investment professionals that we are trying to gain an edge in the market, that often, or very often, we’ll be betting against that consensus herd mentality to achieve abnormal returns relative to the market. So that’s our starting point in this part of our process.”

“We also challenge some of the consensus narratives in the market which are often observed and which experience has shown can be false; an example being that equity markets are expensive.”

“I don’t know how many of you read the news or keep up with financial markets, but the general narrative is that PE, price to earnings ratios are very high, particularly adjusted price to earnings ratios are high from a historical point of view, and the natural inclination or expectation is that those valuations will revert and go to cheaper levels in the future. So, investors become scared as a whole.”

However, we believe equity markets represent winners and losers, and mean reversion is a strategy better employed in fixed income markets. The bull market in equities appears to have further to go…

“…We’ve seen the 2020 COVID crisis, we’ve seen across 2021-22, the fastest inflation and interest cycle in history. More recently, we’ve seen the Trump tariffs, and we’ve seen the US bomb Iran. And in different times, in isolation, those events may have caused this bull market to stutter or even slip into a bear market, but that hasn’t happened.”

Next Susanne introduced our Panel

Helena Wardle, the CEO and founder of Money Means, and also Chris Blundell, partner at MHA who talked about both how to create and launch an AI startup…

Susanne Chishti:

“…Now I want to invite two speakers to the stage. Chris, to share your expertise on how to reward employees in the most tax-efficient ways and Helena on the practical aspects of starting of growing a business . So maybe if we start with Helena.”

Helena Wardle:

“Hi, I’m Helena Wardle, the founder of Money Means, the first AI financial advisor, so yes, it’s exciting.”

Chris Blundell:

“I’m Chris Blundell, tax partner at MHA. I have been advising on tax matters for more than 30 years, working my way through HMRC, a Big 4 firm and then at MHA, where I have been a partner for the past 15 years. I have a particular focus on share incentives and employment taxes for companies of all sizes, whether a start-up, an OMB, or through to mid-size, international and listed companies.

Where smaller and growing companies are concerned, my approach is to help clients focus on what they do best, running their respective business, knowing that I am helping to support matters around tax planning that benefit the business, such as employee retention and incentivisation, through to aspects of wider financial management.”

Susanne Chishti:

“…Helena, maybe if you give a little bit of an overview of how you launched Money Means and how you developed an AI-led financial Assistant.“

Helena Wardle:

“…Effectively, I saw the challenge with people getting access to financial advice, because… especially when you’re younger, you’re starting out, you’re still building wealth, there’s very few options to get help, and it was common that I was helping people at the later stages of their career. I realised that a lot of the time, people were telling me “I wish I did this sooner”, and the reality is that to help out there, financial advice is not readily accessible to most people.

Only less than 10% of you can easily actually access financial advice, but it’s mind- blowingly important, and I can only say that to you because I have worked with hundreds of clients and used this experience to develop a product which goes a long way to creating a solution.

“…Now the challenge is how to recreate a relational aspect because it’s a lot more than what people think as David described. Financial advisors don’t just tell you where to invest your money, yes it’s a big part of it, but as explained, there are lots of steps in it.

It’s helping you work out, like Google Maps, you are here, you need to get there, how do you actually go there?

And that sort of process in itself is not just shoving funds it into an investment, it’s very personal and very relational.

So, I set out to solve that problem. I’m not and I didn’t want to be a tech entrepreneur. I’m a financial planner by profession, but that’s what I ended up having to do because the solutions didn’t exist. We needed to put robustness into it. because it’s heavily regulated for the right reasons. It needs to get the right outcomes for people. So that process has taken four years.

It’s been a tough journey and it’s been a journey that has been enormously rewarding, using AI, a technology that will disrupt everything that we do. The top use of AI today is therapy. So, for people to think the relational aspect of service industries is not replicable is flawed. We’ve evidenced this because we’ve taken our AI model through the financial advisor qualifications,, the qualifications advisors in the UK have to do, and we’ve benchmarked it against ChatGPT. But, if you ask ChatGPT for advice, if you don’t understand the advice really well, you will judge the responses okay.”

“…The challenge is that it just doesn’t know anything about you, and it’s not going to do any work to find that out, because AI predicts a response that you want to hear and that’s effectively how it works, so we built something to work with the flaws of AI and linked that with other technology solutions as a combined sort of solution.

AI ChatGPT failed the exams; it didn’t pass, which is going to be released in the press tomorrow. However, our AI model, Ada, AI digital advisor, aced it. She scored actually better than human advisors as it has got a lot more power behind it than our brains. There is also the mission behind Ada, to help millions of people actually get good outcomes and help that all make a difference.”

Susanne then asked Chris:

“Coming to you, we’ve got lots of founders here in the room, and we’ve had so many new tech changes in the last few years.”

“Given the changes, can you summarize the best way to launch a business in the world?”

Chris Blundell:

“…I think the best strategy with all businesses is about being clear from the start on the structure in relation to your needs and the journey you hope to take through growth and potentially an exit if that’s what you want. Companies are generally a better way of doing things with numerous benefits compared to being a sole trader or even forming a partnership.”

“Partnerships have their place, whether limited or unlimited, but on the whole, most people choose companies because companies are the best way forward.”

Companies provide you with protection as an investor and as an owner; your losses are limited to what you put into the company. Also, the tax rate in a company is lower than it would be for an individual. As a sole trader or as a partner in a partnership, like me, you will be paying 45% tax and national insurance on top of that on your earnings.

In a company, the rate of tax on the company itself, corporation tax, is 25%. Admittedly, once the company makes profits, those profits are in the company, and the next trick is how to get the money out of the company in such a way as to be tax-efficient. While it’s in the company, the best way forward is always to claim all the expenses that you can.”

“…So, whether the expenses you are claiming are capital allowances and the annual investment allowance, that’s a 100% claim in both cases on anything you want to, any tech, any equipment that you purchase, you can set it off against the business profits. And even if you’re making a loss, don’t worry about that because the capital allowances can be carried forward to a future year to be offset against future profits as and when you make them.”

“In terms of other things to do, as David mentioned, putting money into a pension is a good way, once you’re making profits. Rather than paying tax on the profits, use some of the profit to pay into a pension plan up to the £60,000 annual limit. Yes, the money is then tied up in a pension, and that has downsides, such as not being able to access your pension until the age of 57 from 2028, but on balance, it is tax-efficient for both the company and yourself with tax relief up to 45% on your contributions.

“Remember also that Inheritance Tax (IHT) is going to be due on pensions from 2027, however and as the speakers have said, you still need some certainty in an uncertain world and a pension will be part of that.”

Chris continued:

“…I hear many people, even in businesses, talking about “I’ve got a house, that’s going to be my pension, I’ll sell the house and that will be my pension.” – Yes, that’s a possibility, but surely the better way of doing it is putting money into something like an exchange-traded fund that Paul was talking about earlier.”

“…It will grow and as it grows you will end up finding with compound growth, that will become a hugely valuable asset to you in time by the time of your retirement, provided you don’t have to pay IHT on it. It’s early days yet as to what the strategy will be post 2027 to minimise IHT on your pension fund”

“OK, let’s move on to how best to exit a business”

“… If you chose a company structure as a starting point, you will have shares and this will mean that if and when you come to sell them, this will crystallise a capital gain, whether you sell to a third-party buyer, an employee ownership trust or another director, etc.

Capital gains tax rates are at the rate of 24% at the moment. They’ve gone up from 20% and if you qualify for what used to be known as entrepreneurs relief, now business asset disposal relief, essentially for an unquoted company, the shares will qualify for a reduced tax rate that is now 14%, but only for this year; it will be going up to 18% next year, but nonetheless still better than 24%.”

So having shares is the best thing where an exit is concerned.”

Susanne: What other things can you do?

Chris:

“Well, liquidating the company is another option, especially if you built up value in the company. However, this is also a capital gains taxable event. Other than that, extracting money as you’re going along in a tax efficient way has largely been legislated out of existence in so much as the rate of tax on dividend income has been ramped up over the years.

How do I get my money out?

You can get it out, either as a salary or bonus. However, this is going to be taxed at an effective rate of 50-odd percent % when you take into account the kind of interplay between corporation tax relief and what you’re going to be taking out.

Similarly with a dividend, it is the same thing, it’s around about 55% as the effective rate.

A better solution would be to take out money as either interest, for example, if you loan money into the company, then you take the interest out. Yes, the interest on that loan is still taxed at 45%, but it’s obviously better than 54%.

Or consider rent, so if you allow your company to use premises that you have acquired, you can charge a rent to the company, that is again more tax efficient than taking salary out or taking other things out.”

Susanne:

“So now we’re coming to one topic, I know which is very important to all of you who are CEOs and who’ve got employees and team members below you. Which is:

Q: How can the company reward its employees and founders in the most tax-efficient way in terms of bonuses, employee benefits, options, shares?

I wanted to ask Helena first in terms of how do you do it in practice, because you’ve got a large team. We just talked about your great tech developers.

Q: How do you keep your team motivated and incentivised?”

Helena Wardle:

“…I pay them well, it’s the first important point. We pay close or as close to market rates as we can. The one thing I can share is we’ve been running for 4 years and we’ve only just issued the share option.”

“Before I started the business, I pretty much interviewed as many founders as I could find who would give me time and I asked them to tell me all the mistakes they made and share options and giving them too early, giving too many was one that all of them told me.”

“I have not been stingy, I’ve just been very careful. During your first 3, 4, 5 years of your business, you’re very likely to fail. I’m sorry to say that, but that’s true because statistics show that. Startups are not worth anything once they’ve got going, until they get revenue. So do not give share options out. In my opinion, and in my experience, until you have revenue or you reach revenue, you’re giving something away, options, that are almost worth nothing.”

“… That is what I’ve learned, and that’s what I think is really important that I learned from other founders. So, you can do share options, and if you incentivise people early, do that because they’re going to be in your business until you exit. That is actually rare to find, so unless it’s a co-founder, that’s not actually that easy.”

“…Even employee number one, I wouldn’t throw shares at them because they don’t value it. They value it once they can see the business will have a route to succeeding. That’s what I’ve learned from my team and you get their buy-in. So, we talked through share options and how they work, what it actually means to the team before we issued it and to really understand if they value it. Even now I would say half my team do, the rest don’t. This has been the first lesson I’ve learned; pay people well because that’s what they’re there for.”

“But also, the other thing I think is really interesting is that you need to give people opportunities to progress. We are working with really cutting edge tech. Every single person in our business is AI first, which means they use AI to enhance their jobs. They are learning more from our business than any other job they would have. That is enormously valuable to people.”

“…So understand what value you’re adding to your employees. It’s not always mandatory. Are you giving them a learning opportunity they will not find anywhere else? And if you are, there’s big value to it. And people will take salary cuts for that, like two senior leaders have. You know, they may accept an under-market salary rate because they are learning more than they will ever learn in any other business. So that’s really valuable.”

“…The other thing is normal employee benefits, like the stuff we have talked about, is not expensive. We have got really strong benefits. We have sick pay and income protection which costs little but is very attractive. We have death in service, which is really rare for a startup at our stage and again it doesn’t cost us the earth, it’s almost no money.

“We also make sure that we talk about employee benefits and really explain it to the team, and we issue valuations for the share options, because if you can’t put a value to them, what are they actually having? People don’t buy into it if they can’t see what’s in it for them, and you have to bring that to life.

That’s definitely my experience and also that of more than ten founders I spoke to. Be very careful with issuing options too quickly.”

Susanne:

“…Fantastic advice, Helena. Thank you. And maybe if I can ask Chris now. So let’s assume you know you want to launch, it’s at the right time of the startup.

Q: How do you do it? Actually, how do you launch options and share options in the most tax efficient way?”

Chris Blundell

“…I think it is about communicating with your employees. It does not have a magic result with your employees if you give them shares or share options to motivate and incentivise them. They need to understand what they are and what they do and how their efforts can influence their value. If they do understand what they have and you have regular communications with them about their shares’ value, they will be motivated by them and fully understand how their efforts influence the value of their shares over the longer term. So, they are then a win-win for growth and loyalty”

“By giving employees a real stake in the company’s success, share schemes align their financial interests directly with the shareholders’ value, fostering a vital sense of ownership and commitment”

“But what about the tax advantages?”

The primary appeal lies in the generous tax reliefs offered by HMRC-approved schemes, effectively turning future gains into a powerful incentive. This is achieved by allowing employees to avoid or defer high-rate Income Tax and National Insurance Contributions (NICs) on the value of the shares, instead subjecting the profit to the lower Capital Gains Tax (CGT) rate which will be 18% from 2026/27 in an EMI scheme and 24% in the other HMRC approved option schemes. There’ll potentially be no tax at all if you adopt a Share Incentive Plan.

What are the different types of schemes?

- EMI Schemes (Enterprise Management Incentives): The most generous option, designed for smaller, high-growth companies with less than 250 employees and less than £30m of assets on their balance sheet. Employees typically pay no Income Tax or NICs on the grant or exercise of the options. Crucially, the final sale can often qualify for Business Asset Disposal Relief (BADR), taxing the gain at just 18% (on qualifying amounts from 2026/27). This is the gold standard for attracting and retaining key individuals in high-growth firms.

- CSOPs (Company Share Option Plans): A flexible alternative, often used by companies that are too large to qualify for EMI. Employees pay no Income Tax or NICs if the option is exercised at least three years after grant. The eventual gain is subject to CGT.

- SIPs (Share Incentive Plans): Designed for broad employee participation. These are highly tax-efficient: shares (Free, Partnership, or Matching) are generally free of Income Tax and NICs on award, and employees pay no CGT on sale if the shares have been held in the plan for at least five years. This is the top choice for creating an all-employee ownership culture.

Susanne asked Chris how do these schemes help motivation and retention?

“Beyond tax, the structured nature of these schemes makes them excellent retention tools:

- Retention: Options (EMI/CSOP) often include a vesting period (e.g., three to five years). Employees must remain with the company to receive the full benefit, acting as a powerful set of 'golden handcuffs' for key staff.

- Motivation: Employees who are also shareholders are more likely to be engaged, productive, and focused on long-term performance, as they know their hard work directly increases the value of their own shares.

- Recruitment: Offering equity, especially the highly regarded EMI options, can be a crucial competitive advantage for attracting top talent, particularly when cash compensation might be limited.

“By choosing the right scheme—discretionary options for key individuals (EMI, CSOP) or an all-employee plan for broad engagement (SIP)—a UK company can strategically invest in its people and its future growth.”

MHA Wealth is the trading name of MHA Wealth Ltd, a company registered in England (1916615) with registered office at The Pinnacle, 150 Midsummer Boulevard, Milton Keynes, MK9 1LZ. MHA Wealth is authorised and regulated by the Financial Conduct Authority (FCA) with registered number 143715 and is a member of the London Stock Exchange. MHA Wealth is a member of the MHA group. Further information on the MHA group can be found at here.

This communication is for general information only, is a marketing communication, and is not intended to be individual investment advice, a recommendation, tax, or legal advice. The views expressed in this article are those of MHA Wealth or its staff and should not be considered as advice or a recommendation to buy, sell or hold a particular investment or product. In particular, the information provided will not address your personal circumstances, objectives, and attitude towards risk.

Enterprise Investment Schemes (EISs) and Seed Enterprise Investment Schemes (SEIS) are very high-risk investments. Don’t invest unless you’re prepared to lose all the money you invest. These are a high risk investments and you are unlikely to be protected if something goes wrong. The tax treatment depends on the individual circumstances and may be subject to change in future. You are recommended to seek professional regulated advice before taking any action.

Make sure you check out the Gallery below:

Thank you once again to the entire community for bringing your positive energy, laughter, and fellowship to the FINTECH Circle Autumn Drinks. Your enthusiasm and genuine connections truly made the occasion a roaring success.

Looking forward to more gatherings and shared moments in the future.

Until then, “Cheers” to the wonderful memories we created together!

The Team at FINTECH Circle

You might also be interested in

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}