Date: April 13 2026

Author: Declan Sheehy, Author of Disruptive Innovation in Financial Services

Most conversations about innovation in financial services begin in the wrong place. They start with the trendy technology: the AI model, the blockchain protocol, the platform play, and work backwards, hoping the business case reveals itself. After 25 years of operating at the C-suite level across regulated financial services, fintech, and alternative investments, I can tell you that the approach fails more often than it succeeds. Not because the technology is wrong, but because the thinking behind it is incomplete.

That is the central argument of my book, Disruptive Innovation in Financial Services, published this month. It is not a book about technology. It is a book about how you build a complete approach to innovation, one that begins in the mind of the leader and the culture of the organisation, runs through strategy and market positioning to revenue and client experience, and ultimately scales inside one of the most regulated environments on earth.

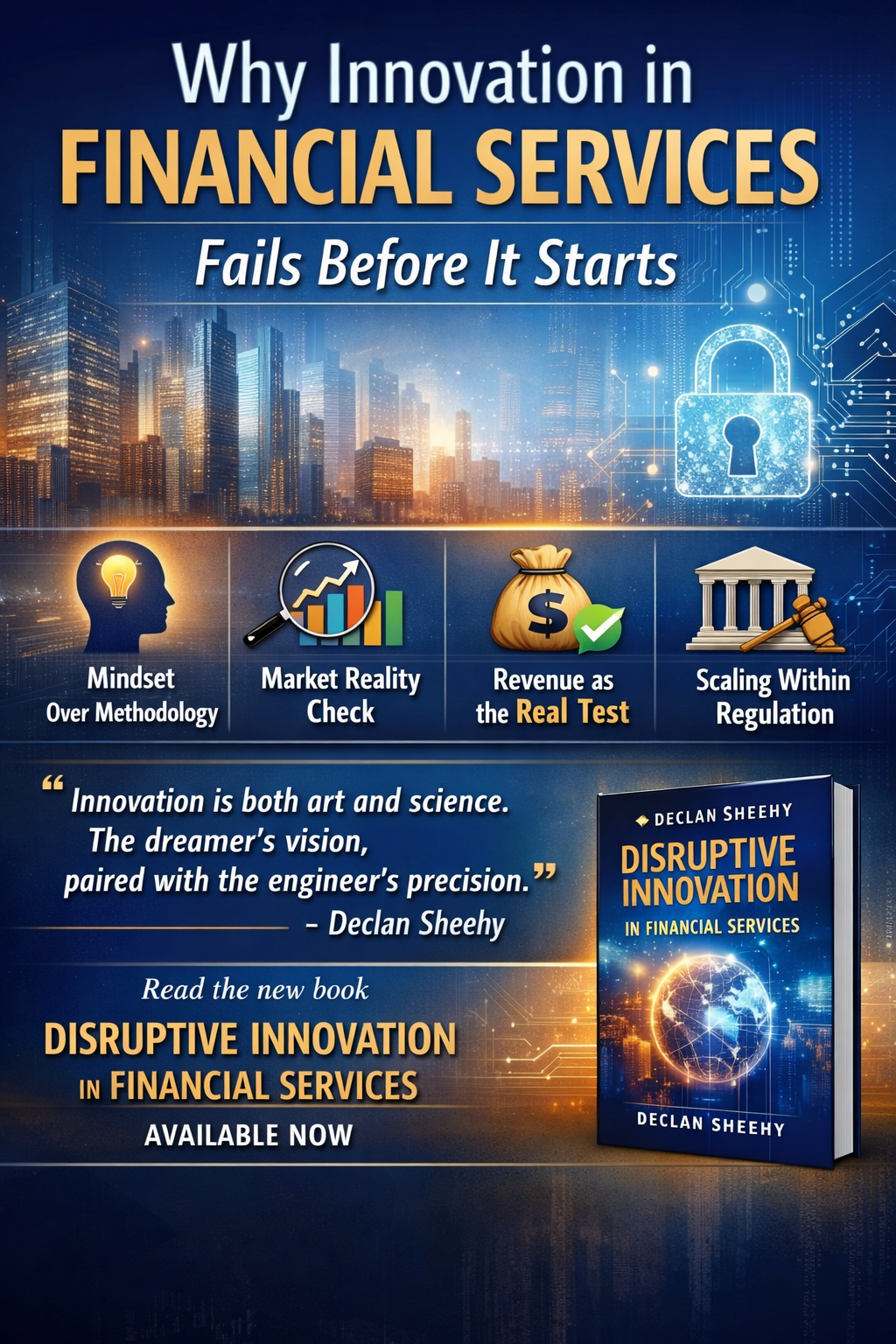

It starts with mindset, not methodology.

The innovator’s mindset is frequently misunderstood. It is not optimism or risk appetite, though both help. It is the ability to be bold, resilient, and curious: to imagine something that does not yet exist, and the discipline to build it within systems designed to resist change. In financial services, those two forces are in constant tension. Regulation, legacy infrastructure, compliance obligations, fiduciary duty. These are not obstacles to innovation. They are the conditions inside which innovation must happen. Leaders who treat them as obstacles tend to move too slowly or break things they should not break.

The firms that get this right, and I draw on Revolut, BlackRock’s Aladdin platform, and Archax throughout the book, treat regulatory discipline not as a constraint on innovation but as a design parameter. They build compliance into the product from the beginning. That shift in thinking changes everything downstream.

Strategy without market reality is just a plan.

Once the mindset is right, the next failure point is the gap between innovation strategy and market truth. I have seen this repeatedly. A leadership team agrees on a direction, then launches into execution without adequately testing whether the market wants what they are building, at the price they intend to charge, through the channel they have chosen. The innovation is internally coherent but externally disconnected.

A good innovation strategy requires understanding where client pain points lie, what emerging paradigms are reshaping the landscape (platform models, ecosystem plays, freemium structures), and how to position your offer so it lands with clarity. These are not marketing questions. They sit at the heart of strategic decision-making and must be addressed before significant capital is deployed.

Revenue is not a consequence of innovation. It is a test of it.

Too many organisations assume commercial outcomes will naturally follow from building a

good product. They will not. Revenue is the market’s verdict on whether your innovation solves a problem worth paying for. Business development in financial services requires a specific kind of discipline: relationship depth, trust built over time, and an understanding of how decisions are actually made within large institutions.

Client experience sits alongside this. In an industry where switching costs are high and trust is hard-won, the client’s experience with your product is also their experience with your brand. Get that wrong, and you are not just losing a deal. You are losing a relationship that took years to build.

Scaling inside regulation is its own discipline.

Growth at scale in financial services is not the same as in other industries. The regulatory environment, FCA, MiFID II, DORA, and evolving AI governance frameworks create obligations that intensify as you grow. What worked as a startup does not automatically survive the scrutiny that comes with institutional scale. I experienced this firsthand, scaling HSBC’s Alternatives division from $200 million in assets under management to $31.6 billion, with zero FCA breaches. That required architecture that could expand without creating compliance risk, and leadership that knew the difference between moving fast and moving recklessly.

AI ethics, open banking ecosystems, platform models, and tokenisation each create genuine opportunities and risks. The firms that navigate this decade well will treat them as interconnected strategic choices.

Why this book, why now?

Financial services are at an inflexion point. The pace of change is not slowing. The regulatory environment is not simplifying. The gap between firms that can innovate at scale and those that cannot is widening. I wrote this book because I have lived that full journey and wanted to give leaders a framework that covers the whole picture.

Innovation is both art and science. The dreamer’s vision, paired with the engineer’s precision. That combination, applied with rigour in one of the world’s most demanding industries, is what separates lasting disruption from mere noise.

Declan Sheehy is an executive leader with 25+ years driving revenue growth, commercial expansion, and operational scale across regulated financial services, fintech, and global alternative investment markets. He has held C-suite mandates at institutions from HSBC to high-growth fintech scaleups. His book, Disruptive Innovation in Financial Services, is available now.

Declan Sheehy is an executive leader with 25+ years driving revenue growth, commercial expansion, and operational scale across regulated financial services, fintech, and global alternative investment markets. He has held C-suite mandates at institutions from HSBC to high-growth fintech scaleups. His book, Disruptive Innovation in Financial Services, is available now.

UK/Ireland: https://www.amazon.co.uk/dp/1919487107

US: https://www.amazon.com/dp/1919487107