Date: December 11 2025

Author: FINTECH Circle

With so many announcements, measures, predictions and revisions included in the UK Autumn Budget, fintech founders, investors, and growth-stage leaders have been left with a simple question: What actually matters to us?

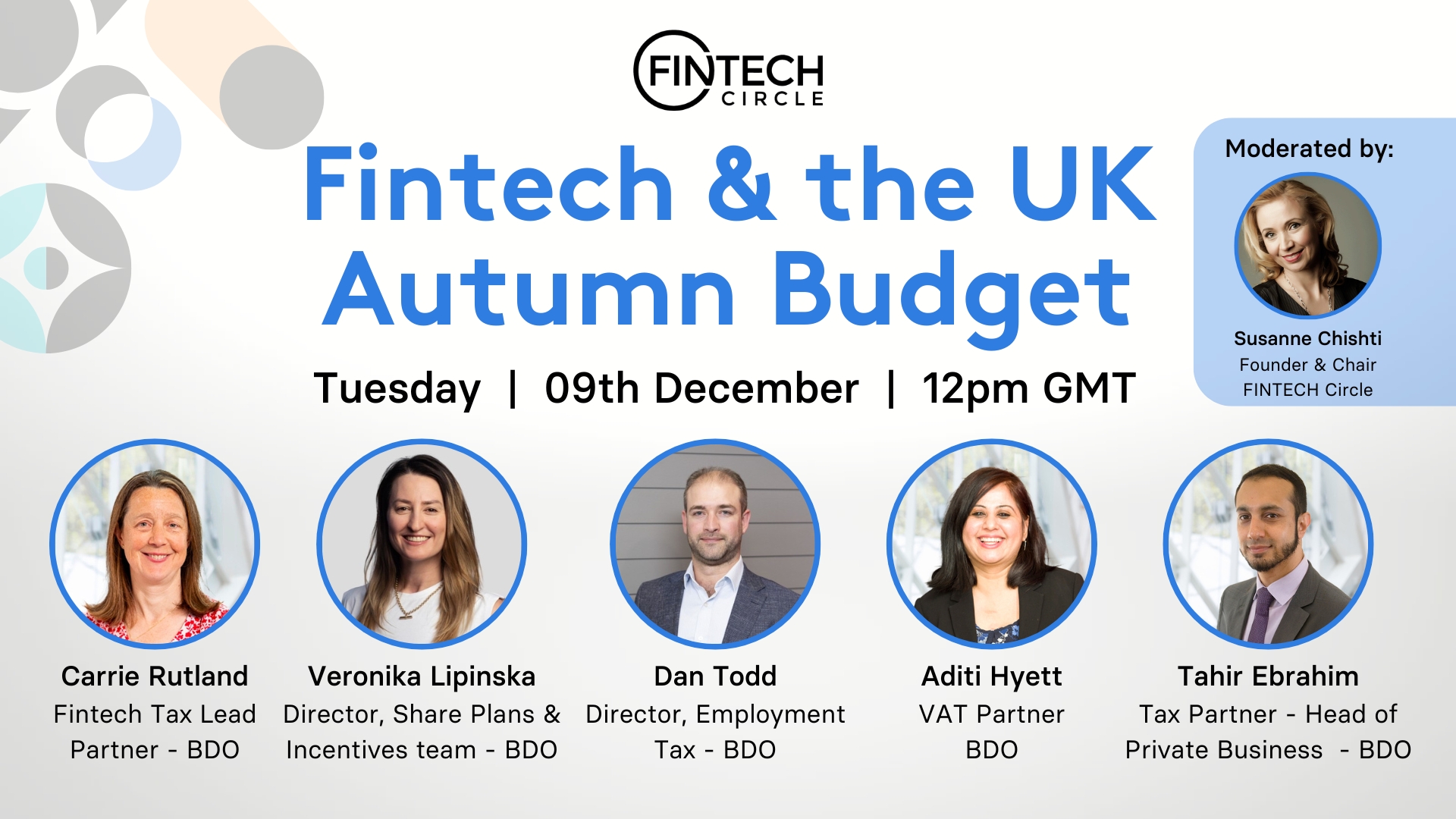

Two weeks after the Chancellor’s announcement, FINTECH Circle hosted a highly practical and insightful webinar to distil exactly that. Moderated by our Founder & Chair Susanne Chishti, the session brought together five senior specialists from BDO to break down the implications of the Autumn Budget for fintech companies—and, crucially, what actions should be taken now to prepare for 2026 and beyond.

Our experts included:

Carrie Rutland – Fintech Tax Lead Partner

Veronika Lipinska – Director, Share Plans & Incentives

Dan Todd – Director, Employment Tax

Aditi Hyett – VAT Partner

Tahir Ebrahim – Tax Partner, Private Business

Together, they delivered a 360° view of corporation tax, incentives, VAT, employment tax, EMI schemes, and personal tax changes—offering fintech leaders the clarity needed to navigate the next phase of regulatory and fiscal change.

1. Corporate Tax & R&D: Stability and Certainty for Founders

Speaker: Carrie Rutland

Carrie opened the session by emphasising one of the most welcome elements of this year’s budget: stability.

Despite industry expectations, corporation tax remains unchanged at 25%, offering predictability for founders planning longer-term investment and expansion. There were also no major changes to R&D tax relief, a relief system that remains vital for early-stage fintechs.

Key updates included:

Capital Allowances (from April 2026):

Writing down allowances reduce to 14%

A new 40% first-year allowance encourages early investment into qualifying assets

Merged R&D Regime: Now fully in effect, with clearer rules and an advanced assurance mechanism available for SMEs

Advanced Assurance for R&D Claims:

Not a full pre-approval, but helpful clarity on:R&D eligibility

Overseas expenditure

Subcontracting rules

PAYE/NIC cap

Government Consultation on Entrepreneurship Incentives:

HMRC is assessing how to redesign the tax system to support founders more effectively. Carrie encouraged fintech leaders to submit feedback—this is a rare chance to influence future policy.

Overall, Carrie highlighted the encouraging sentiment behind the budget: a desire to incentivise entrepreneurship, even if major reforms are still unfolding.

2. VAT: A Simplified Landscape & New Opportunities

Speaker: Aditi Hyett

With numerous rumours circulating pre-budget, many expected sweeping VAT reforms. Instead, the budget delivered fewer—but highly significant—changes.

Key VAT Announcements

A. Major Clarification on VAT Grouping

HMRC confirmed that UK VAT rules take priority, meaning UK businesses no longer need to interpret EU VAT rules when dealing with overseas branches or head offices.

This clarification brings:

Reduced complexity for UK fintechs operating across Europe

Potential VAT refund opportunities for companies that previously followed EU-centric interpretations

The need to update systems and internal processes to align with the UK-focused rules

Aditi emphasised that fintech firms with EU branches should urgently review past positions to identify reclaim opportunities.

B. Future of e-Invoicing

The government confirmed plans to introduce mandatory e-invoicing from April 2029 for B2B and B2G transactions.

This means PDF invoices won’t be sufficient—data must flow digitally between accounting systems.

While immediate action isn’t required, fintech CFOs should ensure ERP providers plan for the transition.

Aditi concluded with a reminder: many fintechs would benefit from a special VAT recovery method, and those without one should reassess their position.

3. EMI Share Option Schemes: Big Wins for Scale-Ups

Speaker: Veronika Lipinska

One of the strongest pro-growth measures in the budget arrived in the form of major enhancements to EMI schemes—a cornerstone incentive for growing fintech teams.

Key EMI Improvements

From April 2026 onwards:

Employee limit increased from 250 to 500

Gross asset limit increased from £30M to £120M

Company-wide EMI option limit increased from £3M to £6M

Option lifespan extended from 10 years to 15 years

EMI notification requirement abolished from April 2027

These changes open EMI eligibility to a significantly broader group of scaling fintechs. For companies that previously outgrew the thresholds, this is a major opportunity to restructure and optimise incentive plans.

Veronika also noted one reduction:

Sales to Employee Ownership Trusts will now incur 12% CGT instead of 0%, though the model remains attractive.

4. Employment Tax: Preparing for Mandatory Benefit Payroll Reporting

Speaker: Dan Todd

Dan addressed several important employment tax changes, including a mix of immediate actions and long-term planning needs.

Salary Sacrifice for Pensions (from April 2029)

A new £2,000 NIC relief cap will apply to salary sacrifice pension contributions above that threshold. This delayed start date gives employers time to adjust—but significant restructuring may be needed.

National Minimum Wage (NMW)

The main NMW rate will increase by 4%, with higher increases for younger employees.

While fintechs historically haven’t faced NMW risk, Dan warned that salary sacrifice for EV schemes, tech equipment or other benefits can push salaries below compliance thresholds.

Payroll of Benefits-in-Kind (BIK) Mandatory from April 2027

One of the biggest HR/payroll changes in years:

All BIKs must be reported via payroll (no more annual P11Ds)

Employers must prepare early—many underestimate the workload

Payroll providers will rely on employer data, so upstream processes must be robust

Expanded Exemptions for Reimbursed Expenses (from April 2026)

Reimbursements for eye tests, flu jabs and homeworking equipment will now also be exempt—good news for employee wellbeing budgets.

5. Personal Tax: Fiscal Drag Continues, But Fewer Shocks Than Expected

Speaker: Tahir Ebrahim

Tahir rounded off the expert updates by exploring personal tax implications—key for founders, investors and senior executives.

Key Personal Tax Measures

Income tax, NIC and inheritance tax thresholds frozen until 2031

→ further fiscal drag likelyDividend, savings and property income tax rates increased by 2%

High-Value Property Surcharge (Mansion Tax)

Applies to homes worth £2M+

Annual charge: £2,500–£7,500

EIS/VCT Rules

Qualifying criteria relaxed

VCT relief reduced from 30% to 20%

May affect investor appetite

Inheritance Tax Business Relief

£1M allowance fixed until 2031

Several anti-avoidance and technical measures introduced

Tahir highlighted what didn’t change—often more important than what did:

No new wealth taxes

No increase to CGT

No CGT-on-exit tax (despite speculation)

PPR and the 7-year IHT gifting rule remain intact

He emphasised the importance of early planning, especially for founders contemplating an exit.

Live Q&A: Practical Founder Concerns Addressed

The session closed with a Q&A covering:

Impact of VCT/EIS changes on capital raising (likely mixed, with rising interest in EIS)

HMRC’s focus areas for R&D inquiries

Real-time VAT reporting (expected eventually, but not soon)

NMW risk in salary-sacrifice-heavy fintechs

EMI eligibility for UK staff of non-UK fintechs (yes, it is possible)

Susanne thanked the audience and the BDO team for bringing welcome clarity to an otherwise complex budget season.

5 Key Takeaways

Stability is the headline: corporation tax and R&D regimes remain unchanged—good news for planning.

EMI improvements are transformational for scaling fintechs—far more companies now qualify.

VAT grouping changes create refund opportunities and reduce complexity for cross-border fintechs.

Mandatory payroll of benefits-in-kind is coming in 2027—planning must begin now.

Personal tax changes reinforce fiscal drag, but avoided the most feared reforms.

Watch the Full Webinar On-Demand below